let's solve it together

Cinema Budgets Dilemma 2024…

“Short Term Urgency v Long Term Strategy”

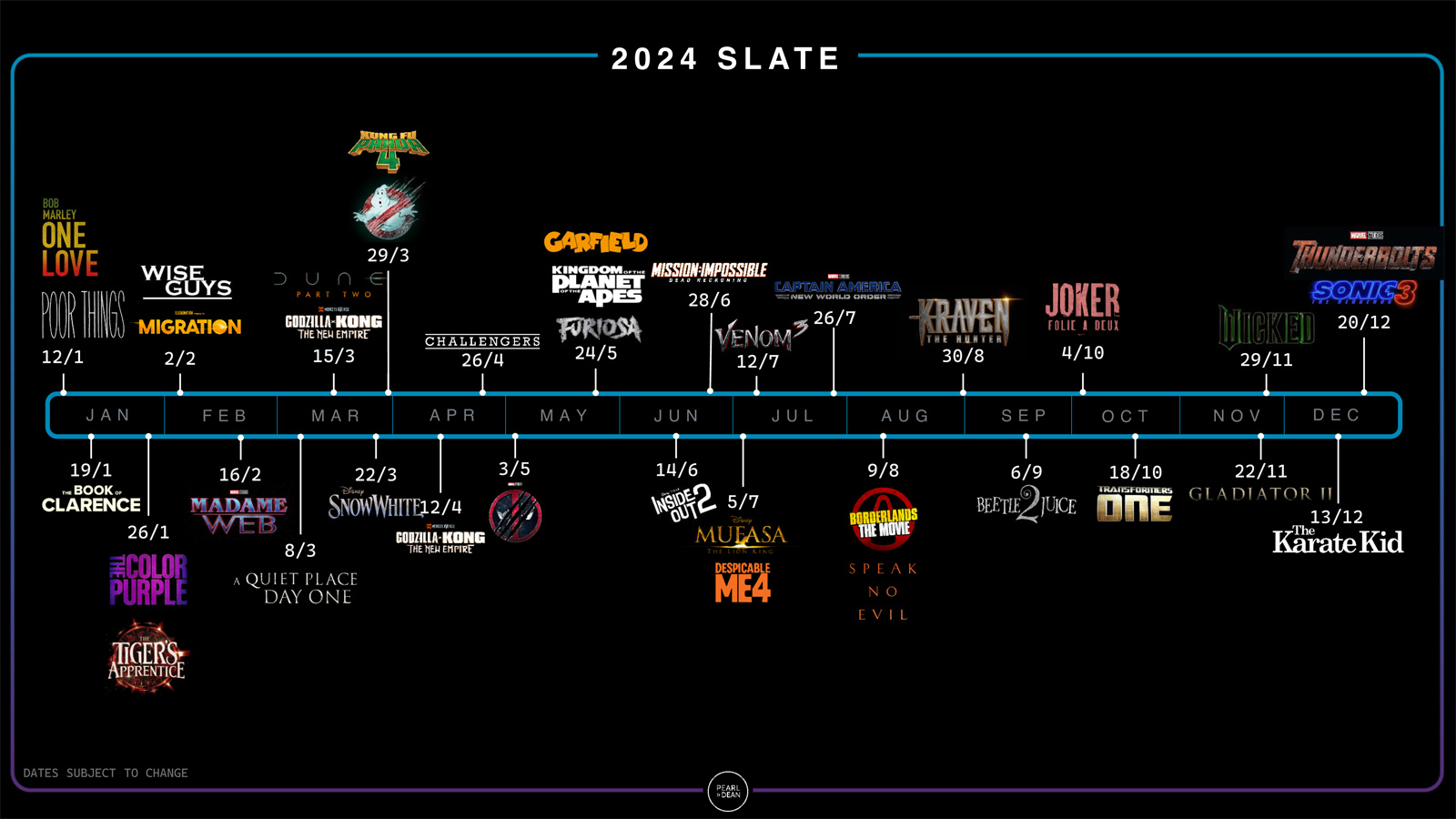

“Besides the marketing challenges the [Hollywood] strike creates, it’s having an impact on the release calendar. First the upcoming GHOSTBUSTERS sequel, KRAVEN THE HUNTER and DUNE: PART TWO were pushed to 2024. Now the issue extends to next year. Multiple tentpoles like the next MISSION IMPOSSIBLE, Pixar’s ELIO and Disney’s SNOW WHITE were just pushed back a year to 2025. As a result of that, 2024 will continue to suffer gaps in the release calendar and a slowdown of the global box office growth”

Link: Gower Street Analytics

The cinema and film marketplaces require to be re-aligned. Today cinema faces highly significant challenges and will have to manage through the volatility created by global events as well as current market specific situations including the fallout from theHollywood strikes, that will continue to include major gaps in the film schedule throughout the remainder of 2023 and 2024.

Link: Sky News - Hollywood Strikes

Studios, investors, shareholders, bond holders, management, landlords, trade suppliers and associations as well as potentially public sector intervention will be required to ensure that market recovery is supported and enabled in the immediate short-term as markets realign to provide the opportunity for long-term strategic planning.

The continual movement of films out of 2024 because of the Hollywood strikes is not only a budget challenge, but a potential disaster for many already struggling cinema operators.

Link: Deadline - Hollywood Strikes

Going into 2024, and looking beyond the strikes, the global cinema sector is weighed down by indebted businesses that, although they have the capacity to generate cash, can barely service the interest on their loans but not the debt itself after covering increasing cost of operation (payroll, business rates, lease commitments and energy costs in particular). As such, the operators generally depend on creditors such as banks (or, throughout the pandemic the government) for their continued existence, effectively putting them on indefinite life support. Individual companies (but not all) continue to operate while in a perilous and unsustainable financial condition. Survival not Growth is the Priority.

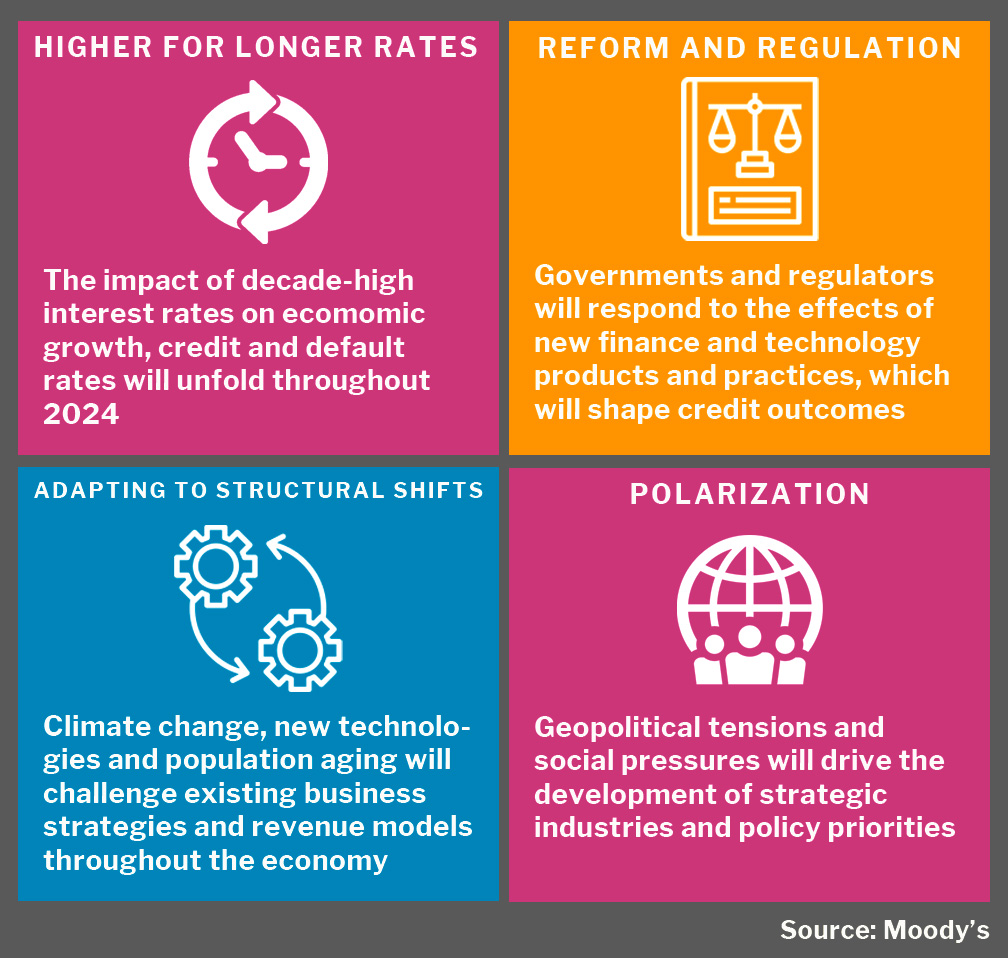

At a Macro Economic level Moody’s highlight, “Four themes that shape the new normal in their 2024 - Adjusting to a new normal driven by rates, geopolitics and technology:

Link: Moody's - Adjusting to a New Outlook

- Central banks will keep rates higher-for-longer to keep a lid on core inflation, which will gradually increase borrowing costs, slow economies, and uncover pockets of risk.

- Structural shifts tied to climate risks, new technologies and demographics will challenge existing business and revenue models.

- Companies will also need to adjust to new reform and regulation in response to financial and social pressures.

- Polarization at the global level will shape industrial policies and investment decisions. At a domestic level, it will slow policy formation.

Moody’s Outlook for Cinema published during 2023 and still current stated that, “Cinema operators have been negatively impacted by the lack of investment in production undertaken by the film studios, and decisions taken by the film studios to cancel or delay content releases to cinemas or to release with a shortened exclusive first release window. Many studios own streaming services and have disrupted conventional exclusive release windows to test the strategic direction and profitability of their own streaming services. Moody's views the lack of consistent studio content releases, particularly for large franchise films, as negatively impacting attendance levels. The weak macro-economic outlook for 2023 [and on-going] places some additional degree of uncertainty around filmgoers' demand. Cinema operators face large, fixed costs associated with long-tenured site leases and are exposed to the inflationary impact of rising energy and staff costs.”

2024 is shaping up to be the most volatile and challenging to be open and operating cinemas ever. Short-term urgency of action will have to take priority over longer-term strategy - it’s budget time!

CFO’s and their Finance departments across the business world have the “Do Not Disturb” signs up and are busy with endless meetings, collecting business critical data, crunching numbers and seeking input into next year’s Budget Plan.

But for cinema market stakeholders and operators, a different sense budget anxiety is lingering throughout the industry. It is one of restlessness…being lost,reported “WTF” outbursts and compliant “No worries, films will be added, it’s always been this way” comments.

Just as shoots of recovery were visible earlier in the year, cinema operators are once again facing another challenge…2024! And most imminently, budgeting for 2024. What happens in production has a knock-on impact all the way through distribution and to point of sale in all businesses, not just cinema.

On reviewing Hollywood dominated film release calendars for 2024 immediate thoughts are to either assume that films have been left off the plan by accident, or to simply stare in disbelief at the predominantly empty pages – not gaps, these are craters! Tent pole releases (the major titles that bring in most customers) such as Disney Pixar’s Elio, Paramount’s Mission Impossible: Dead Reckoning Part 2 and Disney’s Deadpool 3 have already disappeared from the 2024 calendar, due to the SAG-AFTRA actors strike, which halted the production and promotion of Hollywood productions. There will be more moves as ending the strikes is the end of the dispute but not the end of production volatility. The wheels will take time to turn and adjust to the new arrangements. The film release schedule movements is not only a 2024 budget challenge, but a potential commercial disaster for the cinema operators already struggling to survive.

Link: Box Office Mojo - Domestic Release Schedule 2024

Whilst various global box office forecasts for 2024 predicted revenues to be on par with 2023, looking at the currently “confirmed” film releases, would deem that outlook to be highly optimistic. Could 2024 fall short of 2023? Currently there are no #barbenheimer weeks to look forward to.

There is no doubt that in time the calendar gaps will be filled, but the question remains, what will they be filled with? What is going to replace the likes of a Mission Impossible? Are there any finished crowd pulling productions hidden in a secret Hollywood storage vault, ready to be unleashed just for an eventuality such as the one outlined in 2024?

Equally, what if many productions are rushed to completion and enter the market at the same time? This could easily create an over-saturated market for customers (with limited discretionary incomes) having to choose which films to watch on the big screen and which to consume via streaming. Over-saturation of the market will lead to disappointment and for films to under-perform. There has to be a semblance of balance to ensure that the market works effectively.

Even with the Hollywood strikes in resolution, the impacts of it will inevitably lead to a roll-on impact on future productions. Thanksgiving, Americas biggest bank holiday weekend is almost upon us, and the upcoming Christmas period will interrupt production flow into the New Year.

Beyond the film release schedule, cinemasare not immune to geopolitical event impacts, which will result in increased costs of production and logistics; commodities; energy and payroll compounding the inflationary pressures outlined by Moody’s.

Customer cost of living challenges result in more selective customer behaviours so to “just put on a film” is simply not enough anymore. Cinemas will have to become event driven, social and community hubs, to make it “worthwhile” for people to leave the comfort of their homes.

As for the imminent task at hand, compiling a 2024 budget for the entire year seems to be an impossible and meaningless assignment as it stands right now, but key industry stakeholders will base their assessments and financial covenant tests on the plan presented. Never has cinema been more closely scrutinised and under so much recessionary pressure.

Wherever possible, ESS would recommend that rather than attempting to submit and annual plan that Quarterly Survival Budgets, or even 2-monthly Rolling Budget Forecasts are implemented. Aim not to base costs on previous tracking history or rolling three-year averages, because it will not provide a satisfactory output in such a volatile year. The market will need to reset, so basing the budget on break-even or a survival cushion enables the operations to adjust to new norms. Do not overshoot expectations.

Whilst this recommendation is far from ideal, quarterly budgets will allow greater flexibility and, pending on the incoming releases, allow the space to be more pro-active and act to changes in revenue or cost lines immediately, without interruption.

Quarterly budget forecasts will enable more precise staffing planning as well as the roll-on impact of customer service and purchasing decisions. If it is more cost efficient to reduce trading times or hibernate some screens temporarily due to the product issues, take affirmative actions. Closure of under-performing sites should be fast-forwarded and delaying new openings should be considered to ensure that cash within the business is retained. This is not the time to stay precious about maintaining locations for market share’s sake - Bottom Line Sanity v Top Line Vanity.

In the must-read book, Double Your Profits in 6 Months, by Bob Fifer, there is a clear message, “Profitable companies have the money to reward employees, build exciting career paths, and invest in new products, businesses, and technologies. Less profitable companies inevitably sink into mediocrity in all ways – morale, product distinctiveness etc.”

Be prepared to be decisive yet flexible, communicate to the key stakeholders what the actions are (including landlords) as it will make a positive difference. Seek Hardship Relief support wherever available for Property Taxes but be prepared to have your business and trading performance scrutinised (past, present, future) like never before. Solutions can be found, as they were during the pandemic to most issues. A holistic approach, honest and open dialogue, particularly with staff, suppliers, customers, and landlords, generally goes a long way. Recovery for the cinema sector is a Marathon and Not a Sprint.

Cinema is still considered to be one of the most complete art forms, capable of evoking minds, building cultural bridges, inspiring, and being outright fun…a cause truly worthwhile saving.

Entertainment Solution Services Ltd. (ESS) is an international advisory group specialising in the cinema, film production, leisure, and entertainment markets. We have significant global business and development experience working for clients that include government, developers, investors, and operators who require factual insights; growth strategy support or are new market entrants.

ESS cinema sector expertise, knowledge and supportive management has been proven to deliver on core agreed client objectives, enabling a return to sustainability, certainty and stability.

Let’s Solve it Together.